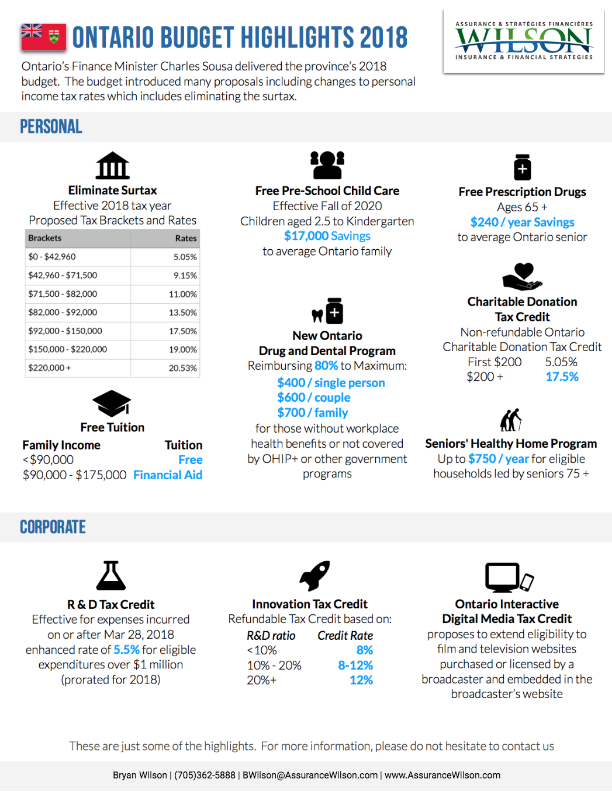

The 2018 Ontario budget features a number of new measures and billions of dollars of enhanced spending across the spectrum, as announced by the province’s Finance Minister, Charles Sousa. Read on for some of the key proposals.

Personal

Eliminate Surtax

A new sliding scale for personal income tax will be introduced, with seven personal income tax rates which will be applied directly to taxable income, in an attempt to eliminate Ontario’s surtax. The province estimates that approximately 680,000 will pay less tax as a result.

Free Tuition

Access to further education will be income linked, with those families with an income of less than $90,000 per year receiving free tuition and families with an income of between $90,000 and $175,00 per year receiving financial aid for tuition costs.

Free Pre-School Child Care

Effective in the Fall of 2020, children aged two-and-a-half until they are eligible for kindergarten can receive free licensed child care.

New Ontario Drug and Dental Program

For those without workplace benefits or not covered by OHIP+, this program offers up to 4.1 million Ontarians a benefit that pays up to 80% of expense up to a cap of $400 for a single person, up to $600 for a couple and $50 per child in a family with two children, regardless of their income.

Free Prescription Drugs

The budget announces the introduction of free prescription drugs for those aged 65 or older, resulting in an average of $240 per year in savings per senior.

Charitable Donation Tax Credit

The non-refundable Ontario Charitable Donation Tax Credit will be tweaked to increase the top rate, remaining at 5.05% for the first $200 but increasing to 17.5% for anything above $200.

Seniors’ Healthy Home Program

$750 is offered to eligible households with seniors of 75 years of age or older to help them to care for and maintain their residence.

Corporate

R&D Tax Credit

The budget introduces a non-refundable tax credit of 3.5% on eligible costs relating to R&D, or an enhanced rate of 5.5% for eligible expenditures of $1 million plus. Note that this enhanced rate would not be payable to corporations where eligible R&D expenditures in the current tax year are less than 90% of eligible R&D expenditures in the tax year before.

Innovation Tax Credit

The existing Ontario Innovation Tax Credit will see changes to its credit rate in the following way:

· If a company has a ratio of R&D expenditures to gross revenues of 10% or less, they will continue to receive the 8% credit.

· If their ratio is between 10% and 20%, they will receive an enhanced credit rate of between 8-12%, calculated on a straight line basis.

· If their ratio is 20% or more, they will receive an enhanced credit rate of 12%.

Ontario Interactive Digital Media Tax Credit

Eligibility to receive this tax credit will be broadened to include film and television websites.

Tax Series: Strategies for Private Corporations

/in blog, corporate, Tax /by Bryan WilsonLast summer, Finance Minister Morneau announced a number of tax reforms for Small Business Owners, including the changes to income sprinkling, minimizing the incentives to keep passive investments and reducing the transfer of corporate surpluses to capital gains.

This year’s Federal Budget focused on tax tightening measures for business owner:

● Small Business Tax Rate Reduction from 10% to 9%.

● Passive Investment Income held within the corp (Reduction begins at $50,000)

● Tax on Split Income

Since these changes will be effective January 1, 2019, a discussion and plan should be prioritized now, since 2018 will be the “prior year” of 2019. Life insurance is a great solution to help business owners address these problems.

Reduced Small Business Tax Rate

● Key Change: Effective January 1, 2019, the small business tax rate will be reduced from 10% to 9%

● Problem: Lower corporate tax rates result in more capital trapped inside the corporation.

● Possible Solution: Life Insurance Proceeds credit the capital dividend account on death allowing for tax-efficient distribution of funds from the corporation to the estate.

Limited Access to Small Business Tax Rate

● Key Change: Passive investment income greater than $50,000/year reduces the small business tax rate limit for small business tax rate. The business limit is reduced to zero at $150,000 of investment income.

● Problem: For companies with passive income over $50,000, the small business limit will be reduced and thus, increase the total amount of tax you have to pay.

● Possible Solution: Exempt life insurance does not produce passive investment income unless there is a disposition. Put a portion of corporations passive investments into a life insurance policy and reduce passive investment income and limit the erosion of the small business limit. Concepts such as Corporate Estate bond, Corporate Insured Retirement Program, Corporate held Critical Illness with Return of Premium

Tax on Split Income

● Key Change: Tax on split income (TOSI) rules extended to cover adult children in certain cases. Different rules depending on age of adult children

● Problem: For adult children receiving income and don’t pass the TOSI rules, income is taxed at the highest personal marginal tax rate on the first dollar. More trapped funds inside the corporation due to fewer tax-effective strategies.

● Possible Solution: Put a portion of corporation’s trapped surplus into a corporate owned life insurance policy which results in tax-efficient distribution of funds from the corporation to the estate.

Ontario Budget 2018

/in blog, Business Owners, corporate, dental benefits, Estate Planning, Family, Group Benefits, Individuals, Investment, Retirees, Tax /by Bryan WilsonThe 2018 Ontario budget features a number of new measures and billions of dollars of enhanced spending across the spectrum, as announced by the province’s Finance Minister, Charles Sousa. Read on for some of the key proposals.

Personal

Eliminate Surtax

A new sliding scale for personal income tax will be introduced, with seven personal income tax rates which will be applied directly to taxable income, in an attempt to eliminate Ontario’s surtax. The province estimates that approximately 680,000 will pay less tax as a result.

Free Tuition

Access to further education will be income linked, with those families with an income of less than $90,000 per year receiving free tuition and families with an income of between $90,000 and $175,00 per year receiving financial aid for tuition costs.

Free Pre-School Child Care

Effective in the Fall of 2020, children aged two-and-a-half until they are eligible for kindergarten can receive free licensed child care.

New Ontario Drug and Dental Program

For those without workplace benefits or not covered by OHIP+, this program offers up to 4.1 million Ontarians a benefit that pays up to 80% of expense up to a cap of $400 for a single person, up to $600 for a couple and $50 per child in a family with two children, regardless of their income.

Free Prescription Drugs

The budget announces the introduction of free prescription drugs for those aged 65 or older, resulting in an average of $240 per year in savings per senior.

Charitable Donation Tax Credit

The non-refundable Ontario Charitable Donation Tax Credit will be tweaked to increase the top rate, remaining at 5.05% for the first $200 but increasing to 17.5% for anything above $200.

Seniors’ Healthy Home Program

$750 is offered to eligible households with seniors of 75 years of age or older to help them to care for and maintain their residence.

Corporate

R&D Tax Credit

The budget introduces a non-refundable tax credit of 3.5% on eligible costs relating to R&D, or an enhanced rate of 5.5% for eligible expenditures of $1 million plus. Note that this enhanced rate would not be payable to corporations where eligible R&D expenditures in the current tax year are less than 90% of eligible R&D expenditures in the tax year before.

Innovation Tax Credit

The existing Ontario Innovation Tax Credit will see changes to its credit rate in the following way:

· If a company has a ratio of R&D expenditures to gross revenues of 10% or less, they will continue to receive the 8% credit.

· If their ratio is between 10% and 20%, they will receive an enhanced credit rate of between 8-12%, calculated on a straight line basis.

· If their ratio is 20% or more, they will receive an enhanced credit rate of 12%.

Ontario Interactive Digital Media Tax Credit

Eligibility to receive this tax credit will be broadened to include film and television websites.

2018 Federal Budget Highlights for Business

/in blog, Business Owners, corporate, Investment, Tax, Uncategorized /by Bryan WilsonThe government’s 2018 federal budget focuses on a number of tax tightening measures for business owners. It introduces a new regime for holding passive investments inside a Canadian Controlled Private Corporation (CCPC). (Previously proposed in July 2017.)

Here are the highlights:

Small Business Tax Rate Reduction Confirmed

Lower small business tax rate from 10% (from 10.5%), effective January 1, 2018 and to 9% effective January 1, 2019.

Limiting Access to the Small Business Tax Rate

A key objective of the budget is to decrease the small business limit for CCPCs with a set threshold of income generated from passive investments. This will apply to CCPCs with between $50,000 and $150,000 of investment income. It reduces the small business deduction by $5 for each $1 of investment income which falls over the threshold of $50,000. This new regulation will go hand in hand with the current business limit reduction for taxable capital.

Limiting access to refundable taxes

Another important feature of the budget is to reduce the tax advantages that CCPCs can gain to access refundable taxes on the distribution of dividends. Currently, a corporation can receive a refundable dividend tax on hand (known as a RDTOH) when they pay a particular dividend, whereas the new proposals aim to permit such a refund only where a private corporation pays non-eligible dividends, though exceptions apply regarding RDTOH deriving from eligible portfolio dividends.

The new RDTOH account referred to “eligible RDTOH” will be tracked under Part IV of the Income Tax Act while the current RDTOH account will be redefined as “non-eligible RDTOH” and will be tracked under Part I of the Income Tax Act. This means when a corporation pays non-eligible dividends, it’s required to obtain a refund from its non-eligible RDTOH account before it obtains a refund from its eligible RDTOH account.

Health and welfare trusts

The budget states that it will end the Health and Welfare Trust tax regime and transition it to Employee Life and Health Trusts. The current tax position of Health and Welfare Trusts are linked to the administrative rules as stated by the CRA, but the income Tax Act includes specific rules relating to the Employee Life and Heath Trusts which are similar. The budget will simplify this arrangement to have one set of rules across both arrangements.

Ontario Budget 2017

/in blog, Budget, Business Owners, Employees, Families, Individuals, Tax, Uncategorized /by Bryan WilsonOntario Finance Minister Charles Sousa delivered the province’s 2017 budget on April 27, 2017. The province’s 2017 budget is balanced, with projected balanced budgets for 2018 and 2019.

Corporate Income Tax Measures

No changes to corporate taxes were announced.

Personal Income Tax Measures

No changes to personal taxes were announced.

Please don’t hesitate to contact us if you have any questions.

Federal Budget 2017 Families

/in blog, Budget, Families, Individuals, Tax, Uncategorized /by Bryan WilsonFinance Minister Bill Morneau delivered the government’s 2017 federal budget on March 22, 2017. The budget expects a deficit of $23 billion for fiscal 2016-2017 and forecasts a deficit of $28.5 billion for 2017-2018. Find out what this means for families.

Read more

Federal Budget 2017Business

/in blog, Budget, Business Owners, Tax, Uncategorized /by Bryan WilsonFinance Minister Bill Morneau delivered the government’s 2017 federal budget on March 22, 2017. The budget expects a deficit of $23 billion for fiscal 2016-2017 and forecasts a deficit of $28.5 billion for 2017-2018. Find out what this means for businesses.

Read more

Corporate Estate Bond

/in blog, Business Owners, Business Owners, Families /by Bryan WilsonWith the end of the year approaching, it’s a good time to look at ways to improve your tax position for 2016. To help you with this, we have prepared a checklist.

As always, please consult us prior to implementing any of these strategies.

Year End Tax Tips

/in blog, Business Owners, Business Owners, Families /by Bryan WilsonWith the end of the year approaching, it’s a good time to look at ways to improve your tax position for 2016. To help you with this, we have prepared a checklist.

As always, please consult us prior to implementing any of these strategies.

Long Term Care Insurance

/in Business Owners, Families, Insurance, Investment, Maturing Families, Preparing for Retirement, Retirees /by Bryan WilsonDid you know that your changes of living to 100 years old are better than ever? While living a long life may be seen as a great gift, we also need to be prepared financially to pay for your future long-term care needs.

Read more

Sources of Funds for Education

/in blog, Education, Investment, RESP /by Bryan WilsonPost-secondary education can be expensive, however having the opportunity to plan for it helps with making sure that you’re capable to meet the costs of education. In addition, when you have a plan, it’s easer to make financial decisions that align with your goals and provide peace of mind. We outline 7 sources of funds for paying for post-secondary education.